こちらの資料がソース。 rstudio-pubs-static.s3.amazonaws.com https://dss.princeton.edu/training/Panel101R.pdf

plmパッケージ

rdrr.io https://cran.r-project.org/web/packages/plm/plm.pdf

データの読み込み

library(foreign)

Panel <- read.dta("http://dss.princeton.edu/training/Panel101.dta")

データ

head(Panel)

country year y y_bin x1 x2 x3 opinion op 1 A 1990 1342787840 1 0.2779036 -1.1079559 0.28255358 Str agree 1 2 A 1991 -1899660544 0 0.3206847 -0.9487200 0.49253848 Disag 0 3 A 1992 -11234363 0 0.3634657 -0.7894840 0.70252335 Disag 0 4 A 1993 2645775360 1 0.2461440 -0.8855330 -0.09439092 Disag 0 5 A 1994 3008334848 1 0.4246230 -0.7297683 0.94613063 Disag 0 6 A 1995 3229574144 1 0.4772141 -0.7232460 1.02968037 Str agree 1

プロット

変数yに関してのプロット。

coplot(y ~ year|country, type="l", data=Panel) # Lines coplot(y ~ year|country, type="b", data=Panel) # Points and lines

散布図。

library(car) scatterplot(y~year|country, boxplots=FALSE, smooth=TRUE, reg.line=FALSE, data=Panel)

固定効果モデル

共分散モデル、Within推定量、個体ダミー変数モデル、最小二乗ダミー変数モデル

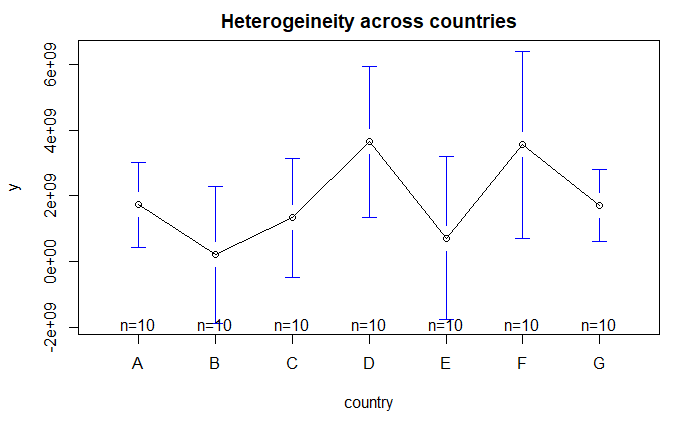

yと国に関しての描画。

library(gplots) plotmeans(y ~ country, main="Heterogeineity across countries", data=Panel)

plotmeansは、平均値の95%信頼区間を描画する。

library(gplots) plotmeans(y ~ year, main="Heterogeineity across countries", data=Panel)

回帰分析

ols <-lm(y ~ x1, data=Panel) summary(ols)

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.524e+09 6.211e+08 2.454 0.0167 *

x1 4.950e+08 7.789e+08 0.636 0.5272

作図

yhat <- ols$fitted plot(Panel$x1, Panel$y, pch=19, xlab="x1", ylab="y") abline(lm(Panel$y~Panel$x1),lwd=3, col="red")

ggplotの場合。

library(ggplot2) ggplot(Panel, aes(x = x1, y = y))+ geom_point() + geom_smooth(method=lm)

重回帰分析・国を追加

fixed.dum <-lm(y ~ x1 + factor(country) - 1, data=Panel) summary(fixed.dum)

Coefficients:

Estimate Std. Error t value Pr(>|t|)

x1 2.476e+09 1.107e+09 2.237 0.02889 *

factor(country)A 8.805e+08 9.618e+08 0.916 0.36347

factor(country)B -1.058e+09 1.051e+09 -1.006 0.31811

factor(country)C -1.723e+09 1.632e+09 -1.056 0.29508

factor(country)D 3.163e+09 9.095e+08 3.478 0.00093 ***

factor(country)E -6.026e+08 1.064e+09 -0.566 0.57329

factor(country)F 2.011e+09 1.123e+09 1.791 0.07821 .

factor(country)G -9.847e+08 1.493e+09 -0.660 0.51190

yhat <- fixed.dum$fitted library(car) scatterplot(yhat~Panel$x1|Panel$country, boxplots=FALSE, xlab="x1", ylab="yhat",smooth=FALSE) abline(lm(Panel$y~Panel$x1),lwd=3, col="red")

要因変数(国)の各要素は、各国特有の効果を吸収している。予測変数x1はOLSモデルでは有意ではなかったが、一旦国ごとの差異をコントロールすると、OLS_DUM(すなわちLSDVモデル)でx1は有意となる。

固定効果:n 個のエンティティ固有の切片(plmパッケージを使用)

y: 従属変数

x1: 独立変数

data: データ

index: パネルセッティング

model="within": 固定効果オプション

library(plm)

fixed <- plm(y ~ x1, data=Panel, index=c("country", "year"), model="within")

summary(fixed)

結果。

Balanced Panel: n = 7, T = 10, N = 70

Residuals:

Min. 1st Qu. Median Mean 3rd Qu. Max.

-8.63e+09 -9.70e+08 5.40e+08 0.00e+00 1.39e+09 5.61e+09

Coefficients:

Estimate Std. Error t-value Pr(>|t|)

x1 2475617827 1106675594 2.237 0.02889 *

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Total Sum of Squares: 5.2364e+20

Residual Sum of Squares: 4.8454e+20

R-Squared: 0.074684

Adj. R-Squared: -0.029788

F-statistic: 5.00411 on 1 and 62 DF, p-value: 0.028892

n = グループ/パネル数

T = 年

N = 総観測数

Coefficients:Estimate

x1の係数は、Xが1単位増加したときに、Yが国ごとに平均してどれだけ時間的に変化するかを示している。

x Pr(>|t|):0.02889:

Pr(>|t|)= 両側p値は,各係数が0と異なるという仮説を検定する。これを棄却するには,p値が0.05 (95%, 0.10のアルファも選択できる)でなければならず、これが事実であれば、その変数が従属変数(y)に有意な影響を持つことができる。

p-value: 0.028892:

この数値が< 0.05であればこのモデルは問題ない。これは、モデルのすべての係数が0に比べて異なるかどうかを見る検定(F)である。

fixef(fixed) # 固定効果(各国の定数)を表示する

結果。

A B C D E F G 880542404 -1057858363 -1722810755 3162826897 -602622000 2010731793 -984717493

pFtest(fixed, ols) # 固定効果に対する検定。固定効果よりもOLSの方が良いのか?

結果。

data: y ~ x1 F = 2.9655, df1 = 6, df2 = 62, p-value = 0.01307 alternative hypothesis: significant effects

p値が0.05未満であれば、固定効果モデルがより良い選択となる。

ランダム効果モデル (ランダム切片, 部分プーリングモデル)

model="random"と指定する。

random <- plm(y ~ x1, data=Panel, index=c("country", "year"), model="random")

summary(random)

結果。

Balanced Panel: n = 7, T = 10, N = 70

Effects:

var std.dev share

idiosyncratic 7.815e+18 2.796e+09 0.873

individual 1.133e+18 1.065e+09 0.127

theta: 0.3611

Residuals:

Min. 1st Qu. Median Mean 3rd Qu. Max.

-8.94e+09 -1.51e+09 2.82e+08 0.00e+00 1.56e+09 6.63e+09

Coefficients:

Estimate Std. Error z-value Pr(>|z|)

(Intercept) 1037014284 790626206 1.3116 0.1896

x1 1247001782 902145601 1.3823 0.1669

Total Sum of Squares: 5.6595e+20

Residual Sum of Squares: 5.5048e+20

R-Squared: 0.02733

Adj. R-Squared: 0.013026

Chisq: 1.91065 on 1 DF, p-value: 0.16689

係数の解釈は難しい。なぜなら、係数はwithin効果とbetween果の両方を含んでいるからである。TSCSの場合、Xが時間軸で1単位、国別で1単位変化したときのXのYに対する平均的な効果を表している。

Pr(>|t|)= 両側検定のp値は,各係数が0と異なるという仮説を検定する。これを棄却するには,p値が0.05 (95%, 0.10のアルファも選択できる)でなければならず,これが事実であれば,その変数が従属変数(y)に有意な影響を持つことができる.

カイ二乗検定のP値:この数値が<0.05であれば、そのモデルはOKである。これは、モデル中のすべての係数がゼロと異なるかどうかを確認する検定 (F)である。

パネルデータとして設定(上記のモデルを実行する別の方法)

Panel.set <- pdata.frame(Panel, index = c("country", "year"))

plmパッケージでは、plm.data()はpdata.frame()に変更されている。

パネル設定によるランダム効果 (上記と同じ出力)

random.set <- plm(y ~ x1, data = Panel.set, model="random") summary(random.set)

結果。

Balanced Panel: n = 7, T = 10, N = 70

Effects:

var std.dev share

idiosyncratic 7.815e+18 2.796e+09 0.873

individual 1.133e+18 1.065e+09 0.127

theta: 0.3611

Residuals:

Min. 1st Qu. Median Mean 3rd Qu. Max.

-8.94e+09 -1.51e+09 2.82e+08 0.00e+00 1.56e+09 6.63e+09

Coefficients:

Estimate Std. Error z-value Pr(>|z|)

(Intercept) 1037014284 790626206 1.3116 0.1896

x1 1247001782 902145601 1.3823 0.1669

Total Sum of Squares: 5.6595e+20

Residual Sum of Squares: 5.5048e+20

R-Squared: 0.02733

Adj. R-Squared: 0.013026

Chisq: 1.91065 on 1 DF, p-value: 0.16689

固定効果がランダム効果か?

固定効果かランダム効果かを決定するために、帰無仮説は、望ましいモデルがランダム効果で、代替モデルが固定効果であるとするHausman検定を実行できる(Green, 2008, chapter 9を参照)。 これは基本的に、固有誤差(ui)が回帰変数と相関しているかどうかを検定するもので、帰無仮説は相関していないというものである。

固定効果モデルを実行して推定値を保存し、次にランダム・モデルを実行して推定値を保存し、そして検定を実行する。P値が有意であれば(たとえば、<0.05)、固定効果を使用し、そうでなければランダム効果を使用する。

phtest(fixed, random)

結果。

Hausman Test data: y ~ x1 chisq = 3.674, df = 1, p-value = 0.05527 alternative hypothesis: one model is inconsistent

p-valueの数値が0.05未満であれば、固定効果を用いる。

その他のテスト・測定項目

時間固定効果に対する検定

fixed <- plm(y ~ x1, data=Panel, index=c("country", "year"), model="within")

fixed.time <- plm(y ~ x1 + factor(year), data=Panel, index=c("country", "year"), model="within")

summary(fixed.time)

結果。

Coefficients:

Estimate Std. Error t-value Pr(>|t|)

x1 1389050354 1319849567 1.0524 0.29738

factor(year)1991 296381559 1503368528 0.1971 0.84447

factor(year)1992 145369666 1547226548 0.0940 0.92550

factor(year)1993 2874386795 1503862554 1.9113 0.06138 .

factor(year)1994 2848156288 1661498927 1.7142 0.09233 .

factor(year)1995 973941306 1567245748 0.6214 0.53698

factor(year)1996 1672812557 1631539254 1.0253 0.30988

factor(year)1997 2991770063 1627062032 1.8388 0.07156 .

factor(year)1998 367463593 1587924445 0.2314 0.81789

factor(year)1999 1258751933 1512397632 0.8323 0.40898

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Total Sum of Squares: 5.2364e+20

Residual Sum of Squares: 4.0201e+20

R-Squared: 0.23229

Adj. R-Squared: 0.00052851

F-statistic: 1.60365 on 10 and 53 DF, p-value: 0.13113

個体効果および時間効果に関するF検定 F Test for Individual and/or Time Effects

withinモデルとpoolingモデルの比較に基づく個人効果および時間効果の検定。

pFtest(fixed.time, fixed)

結果。

F test for individual effects data: y ~ x1 + factor(year) F = 1.209, df1 = 9, df2 = 53, p-value = 0.3094 alternative hypothesis: significant effects

この数値が<0.05であれば 時間固定効果を用いる。この例では、時間固定効果を使用する必要はない。

パネルモデルに対するラグランジュFF乗数検定 Lagrange FF Multiplier Tests for Panel Models

パネルモデルにおける個人効果および時間効果の検定である。

plmtest(fixed, c("time"), type=("bp"))

Lagrange Multiplier Test - time effects (Breusch-Pagan) for balanced panels data: y ~ x1 chisq = 0.16532, df = 1, p-value = 0.6843 alternative hypothesis: significant effects

この数値が<0.05であれば 時間固定効果を用いる。この例では、時間固定効果を使用する必要はない。

ランダム効果に対する検定 Breusch-Pagan ラグランジュ乗数(LM)

pool <- plm(y ~ x1, data=Panel, index=c("country", "year"), model="pooling")

summary(pool)

結果。

Residuals:

Min. 1st Qu. Median Mean 3rd Qu. Max.

-9.55e+09 -1.58e+09 1.55e+08 0.00e+00 1.42e+09 7.18e+09

Coefficients:

Estimate Std. Error t-value Pr(>|t|)

(Intercept) 1524319070 621072624 2.4543 0.01668 *

x1 494988914 778861261 0.6355 0.52722

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Total Sum of Squares: 6.2729e+20

Residual Sum of Squares: 6.2359e+20

R-Squared: 0.0059046

Adj. R-Squared: -0.0087145

F-statistic: 0.403897 on 1 and 68 DF, p-value: 0.52722

LM検定は,ランダム効果回帰と単純なOLS回帰のどちらかを決定するのに役立つ。

LM検定での帰無仮説は,実体間の分散が0であるということである。これは,単位間の有意な差がない(すなわち,パネル効果がない)ことを意味する。

plmtest(pool, type=c("bp"))

Lagrange Multiplier Test - (Breusch-Pagan) for balanced panels data: y ~ x1 chisq = 2.6692, df = 1, p-value = 0.1023 alternative hypothesis: significant effects

ここでは、帰無値を棄却できず、ランダム効果が適切でないと結論づけられた。これは、国による有意差の証拠がない 国による有意差の証拠がないため、単純なOLS回帰を実行することができる。

Breusch-Pagan LMの独立性検定とPasaran CD検定による横断的依存性/同時発生的相関の検定

Baltagiによれば,クロスセクション依存性 cross-sectional dependence は,長い時系列を持つマクロパネルでは問題である。これは,ミクロ・パネル(数年,多数のケース)では,あまり問題にならない.

独立性のB-P/LM検定とPasaran CD検定における帰無仮説は,主体間の残差は相関しないことである。 B-P/LMおよびPasaran CD(断面依存性)検定は,残差がエンティティ間*で相関しているかどうかを検定するために使用される.クロスセクション依存性は,検定結果にバイアスをもたらす可能性がある(同時計数相関 contemporaneous correlation ともいう)。

*Source: Hoechle, Daniel, “Robust Standard Errors for Panel Regressions with Cross-Sectional Dependence”, http://fmwww.bc.edu/repec/bocode/x/xtscc_paper.pdf

fixed <- plm(y ~ x1, data=Panel, index=c("country", "year"), model="within")

pcdtest(fixed, test = c("lm"))

結果。

Breusch-Pagan LM test for cross-sectional dependence in panels data: y ~ x1 chisq = 28.914, df = 21, p-value = 0.1161 alternative hypothesis: cross-sectional dependence

pcdtest(fixed, test = c("cd"))

Pesaran CD test for cross-sectional dependence in panels data: y ~ x1 z = 1.1554, p-value = 0.2479 alternative hypothesis: cross-sectional dependence

系列相関の検定

系列相関検定は,長い時系列を持つマクロパネルに適用される。ミクロ・パネル(年数が非常に少ない)では問題ない。帰無仮説は,系列相関がないことである.

pbgtest(fixed)

結果。

Breusch-Godfrey/Wooldridge test for serial correlation in panel models data: y ~ x1 chisq = 14.137, df = 10, p-value = 0.1668 alternative hypothesis: serial correlation in idiosyncratic errors

p-value=0.1668なので、系列相関がない。

単位根/定常性の検定

確率的トレンドを確認するためのDickey-Fuller検定。帰無仮説は、系列が単位根を持つ(すなわち、非定常)ことである。単位根が存在する場合、変数の第1階差を取ることができる。

Panel.set <- plm.data(Panel, index = c("country", "year"))

library(tseries)

adf.test(Panel.set$y, k=2)

結果。

Augmented Dickey-Fuller Test data: Panel.set$y Dickey-Fuller = -3.9051, Lag order = 2, p-value = 0.0191 alternative hypothesis: stationary

p値<0.05の場合、単位根は存在しない。

分散不均一性 heteroskedasticity の検定

library(lmtest) bptest(y ~ x1 + factor(country), data = Panel, studentize=F)

Breusch-Pagan test data: y ~ x1 + factor(country) BP = 14.606, df = 7, p-value = 0.04139

P<0.05であるため分散不均一性 heteroskedasticityが検出された。

分散不均一性が検出された場合、ロバスト共分散行列を使用してそれを考慮することができる。

分散不均一性を制御--ロバスト共分散行列推定法(Sandwich推定法)

vcovHC-関数は、3つの異種分散共分散推定量を推定します。

- "white1" - 一般的な異種分散性を持つが系列相関を持たない場合。ランダム効果に推奨。

- "white2" - "white1 "をグループ内の共通分散に制限したもの。ランダム効果に推奨

- "arellano" - 分散不均一性と系列相関の両方。固定効果に推奨。

以下のオプションが適用される*。

- HC0 - 分散不均一性の整合性。デフォルト。

- HC1,HC2,HC3 - サンプル数が少ない場合に推奨される。HC3は、影響力のあるオブザベーションにあまりきを置かない.

- HC4 - 影響力のあるオブザベーションを持つ小さな標本.

- HAC - 分散不均一性と自己相関の整合性(詳細は, ?vcovHAC とタイプ).

*Kleiber and Zeileis, 2008.

分散不均一性の制御 ランダム効果

random <- plm(y ~ x1, data=Panel, index=c("country", "year"), model="random")

coeftest(random) # 本来の係数 Original coefficients

結果。

t test of coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1037014284 790626206 1.3116 0.1941

x1 1247001782 902145601 1.3823 0.1714

coeftest(random, vcovHC) # 分散不均一性整合係数 Heteroskedasticity consistent coefficients

結果。

t test of coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1037014284 907983029 1.1421 0.2574

x1 1247001782 828970247 1.5043 0.1371

# 分散不均一性整合係数タイプ 3Heteroskedasticity consistent coefficients, type 3 coeftest(random, vcovHC(random, type = "HC3"))

結果。

t test of coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1037014284 943438284 1.0992 0.2756

x1 1247001782 867137585 1.4381 0.1550

係数のHC標準誤差を以下に示す

t(sapply(c("HC0", "HC1", "HC2", "HC3", "HC4"), function(x) sqrt(diag(vcovHC(random, type = x)))))

(Intercept) x1 HC0 907983029 828970247 HC1 921238957 841072643 HC2 925403820 847733474 HC3 943438284 867137584 HC4 941376033 866024033

標準誤差は、HCの種類によって異なる。

分散不均一性の制御・固定効果

fixed <- plm(y ~ x1, data=Panel, index=c("country", "year"), model="within")

coeftest(fixed) # 本来の係数Original coefficients

結果。

t test of coefficients:

Estimate Std. Error t value Pr(>|t|)

x1 2475617827 1106675594 2.237 0.02889 *

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

coeftest(fixed, vcovHC) # 分散不均一性整合係数 Heteroskedasticity consistent coefficients

結果。

t test of coefficients:

Estimate Std. Error t value Pr(>|t|)

x1 2475617827 1358388942 1.8225 0.07321 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

# 分散不均一性整合係数 (Arellano) coeftest(fixed, vcovHC(fixed, method = "arellano"))

結果。

t test of coefficients:

Estimate Std. Error t value Pr(>|t|)

x1 2475617827 1358388942 1.8225 0.07321 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

# 分散不均一性整合係数タイプ 3Heteroskedasticity consistent coefficients, type 3 coeftest(fixed, vcovHC(fixed, type = "HC3"))

結果。

t test of coefficients:

Estimate Std. Error t value Pr(>|t|)

x1 2475617827 1439083523 1.7203 0.09037 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

係数のHC標準誤差を以下に示す

t(sapply(c("HC0", "HC1", "HC2", "HC3", "HC4"), function(x) sqrt(diag(vcovHC(fixed, type = x)))))

結果。

HC0.x1 HC1.x1 HC2.x1 HC3.x1 HC4.x1 [1,] 1358388942 1368196931 1397037369 1439083523 1522166034

パッケージをワークスペースから取り除く。

detach("package:gplots")